Before you even think about applying for a home loan, you need to understand one thing: the bank’s most important document isn’t your pay slip. It’s your credit report.

Here’s the biggest myth to clear up right away: many people think having no debt makes them a perfect borrower. They have no credit cards, no loans, nothing.

In reality, a “thin credit file” is a red flag. Banks have no history to judge your repayment behavior. They don’t know if you’re financially disciplined or a total mess. This can result in lower loan amounts, tougher conditions, or even rejection.

A healthy credit history—showing you’re responsible with debt—can be a huge asset. So if you’re planning to buy a home, you need to start building your credit profile now.

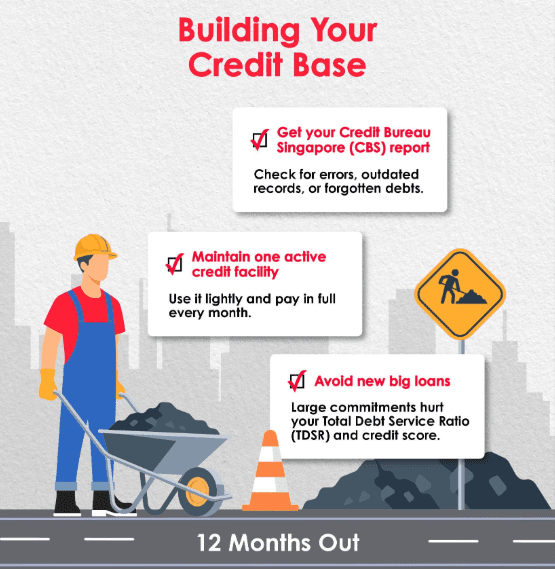

12 Months Out: Laying the Foundation

This is the most crucial stage. Your goal here is to build a solid track record of good financial habits.

- Get Your Credit Report from CBS: This is a non-negotiable first step. Order a copy from Credit Bureau Singapore (CBS) to check for any mistakes, outdated information, or forgotten small debts.

- Open (or Keep) One Credit Facility: If you have no active credit, get a simple credit card. Use it for a small, regular expense like your mobile phone bill and pay it off in full every single month.

- Pay All Bills On Time: This is the golden rule. Set up GIRO for credit cards, utilities, and any other loans to ensure you never miss a due date.

- Reduce Outstanding Balances: Keep your credit card utilization below 30% of your total credit limit. This signals to banks that you are not overly reliant on credit.

- Avoid New Large Loans: Don’t buy a new car or take out a personal loan. These new debts will hurt your Total Debt Servicing Ratio (TDSR) and your credit score.

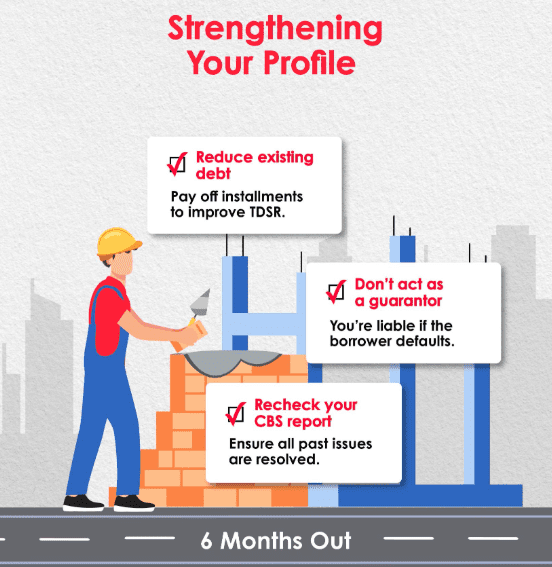

6 Months Out: Polishing Your Profile

At this point, you should have a solid foundation. Now, it’s about optimizing and avoiding any sudden changes.

- Stop Applying for New Credit: This is the most common mistake. Every time you apply for a new credit card or an instalment plan, it creates a “hard inquiry” on your report, which can cause a temporary dip in your score.

- Prepay or Reduce Debts Where Possible: Get rid of high-interest debt, like personal loans, to free up your debt headroom and improve your TDSR.

- Spread Out Card Payments: Don’t wait until the due date to pay off your card. Spreading out payments before the statement date will keep your reported utilization low.

- Avoid Becoming a Guarantor: Signing as a guarantor for someone else’s loan makes you liable if they default, which can severely damage your own credit score.

Check Your CBS Report Again: This is a final check to ensure that any past issues have been corrected and that your profile is clean.

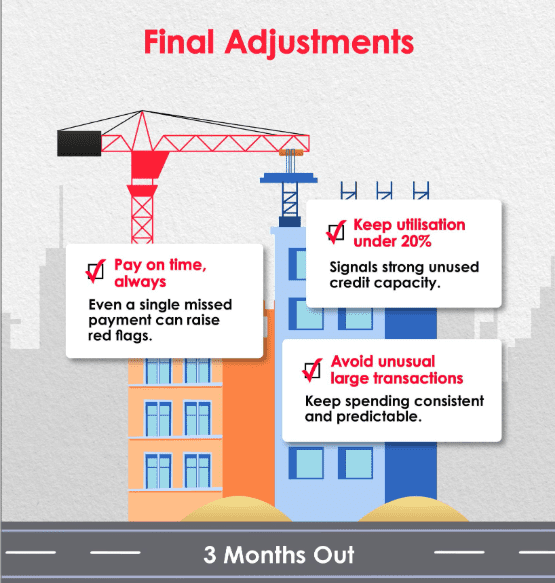

3 Months Out: Fine-Tuning Your Finances

You are in the final stretch. The goal now is stability. You want your profile to look as predictable and low-risk as possible.

- No New Credit Applications: Zero hard inquiries. Stability looks much better to banks than sudden activity.

- Keep Utilization Ultra-Low (<20%): A low utilization rate shows you have plenty of unused credit capacity, which banks love to see.

- Maintain On-Time Payments: No exceptions. Even a small, missed due date can raise a red flag.

- Avoid Unusual Large Transactions: A sudden spending spree can make you look risky. Keep your spending consistent and predictable.

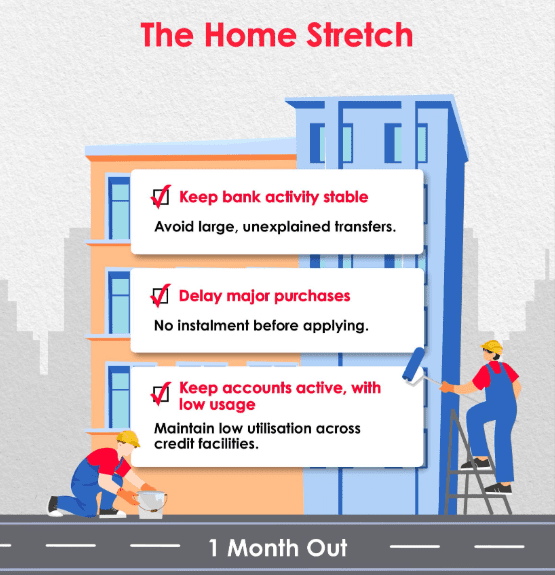

The Final Countdown: 1 Month to Go

This is the final prep. Your actions now are about making sure your report is spotless.

- Stable Bank Account Activity: Avoid big, unexplained transfers in or out of your bank accounts.

- Hold Off on Major Purchases: Do not buy furniture on instalment plans or make any new hire purchases right before your loan application.

- Keep All Accounts Active But Low Usage: Show consistent, responsible behavior right up to the day you apply.

The Bottom Line: A Few Extra Pointers

- TDSR & MSR: Even with a high score, too much monthly debt can cause you to fail these affordability tests. Your credit score gets you in the door, but your income and existing debt determine the final loan amount.

- Joint Applications: The bank will assess both applicants’ scores and use the lower one to determine approval terms. Ensure your co-borrower has a healthy credit profile too.

- Give Yourself Time: If your credit file is thin or you have past issues, budget at least 6 to 12 months to fix it before you even start looking for a property. It’s time well spent.