In Singapore, property is the most powerful wealth-building tool most people will ever have access to. While we’ve seen everything from stocks to crypto explode in recent years, a well-planned property investment offers something few other assets can match: clarity and long-term stability.

Thanks to our government’s long-term planning, the residential property market has consistently shown steady growth. But to truly unlock its potential, especially for a family, you have to think beyond just one home.

The question then is, how do you own multiple properties without overpaying on taxes?

That’s where strategic planning comes in.

The Endgame: How to Own More Than One Property

For households looking to maximize wealth through real estate, owning more than one residential property is the ultimate strategy. But it has to be carefully planned from the start, depending on your life stage.

Stage 1: The Young Couple’s BTO Move

This is the typical starting point for many households in Singapore. Young couples often jointly apply for their first HDB BTO to combine their financial resources and maximize their loan eligibility.

But let’s be clear: Is joint ownership truly necessary?

An alternative, often overlooked approach is for one party—typically the one with the stronger income—to be the sole owner, while the other is listed as an Essential Occupier.

This simple decision upfront offers powerful long-term benefits:

- The Essential Occupier retains their eligibility to purchase a second property.

- No decoupling is required later, avoiding unnecessary costs and complexities.

- The HDB can be kept after the MOP is fulfilled, allowing the couple to own two properties simultaneously.

Note: A crucial point to remember is that decoupling has not been allowed for HDB properties since 2016. This makes the initial ownership structure an even more critical decision.

Stage 2: The Decoupling Play for Private Property

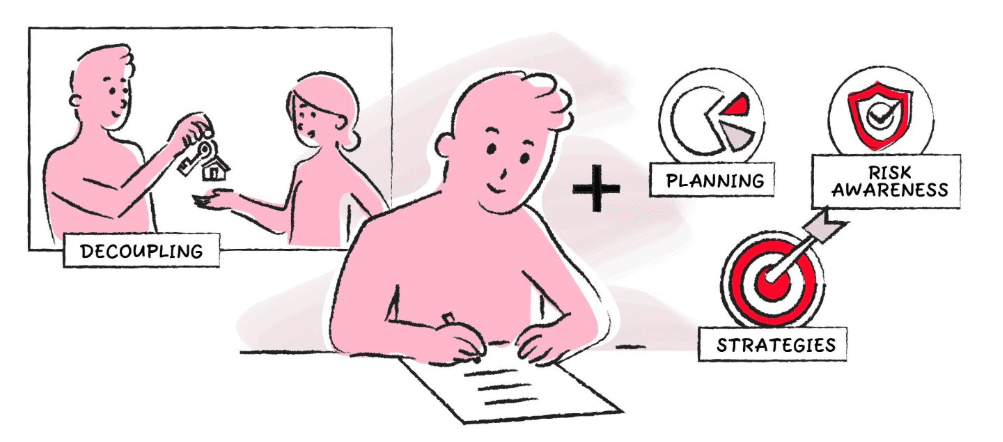

For those who already own a private property jointly, decoupling is still a highly effective strategy to unlock second property ownership without paying an unnecessary tax.

What exactly is decoupling? It’s the legal process of transferring ownership of a property from joint names to a single owner, allowing the other party to purchase another property as a first-time buyer.

Key Considerations Before You Decouple:

- Financial Feasibility: Can the remaining owner take over the full mortgage and monthly repayments on a single income? This is the most important question to answer.

- The Costs: Decoupling isn’t free. You’ll need to budget for:

- Buyer Stamp Duty (BSD) on the transferred share.

- Legal and valuation fees.

- A significant CPF refund obligation (with accrued interest), which may require a cash top-up if the sales proceeds are insufficient.

- The Exit Plan: Does this strategy align with your long-term goals? Are you looking for capital appreciation, rental income, or both?

Final Verdict: Is Decoupling Still a Winning Strategy?

Yes—when used wisely.

Decoupling continues to be a powerful strategic enabler for households to grow their wealth through residential real estate in Singapore. When paired with thoughtful financial planning and a clear understanding of legal and CPF implications, it allows families to build a strong foundation for capital appreciation and rental income.

But remember, it’s just one tool in a wider investment toolkit. Every household should also consider their risk profile and explore other options, from “sell one, buy two” to investing in commercial properties, to diversify and grow their wealth holistically.

In the end, confidence comes not from ignoring the risks but from knowing exactly how to manage them.