Ever been curious about how others handle their mortgages? Or who secures them?

If your answer is yes, then Redbrick is here to help answer your questions! We’ve condensed some of the insights obtained from mortgages we’ve transacted during the first half of this year, in order to give you a glimpse into the goings-on within the local mortgage market.

__

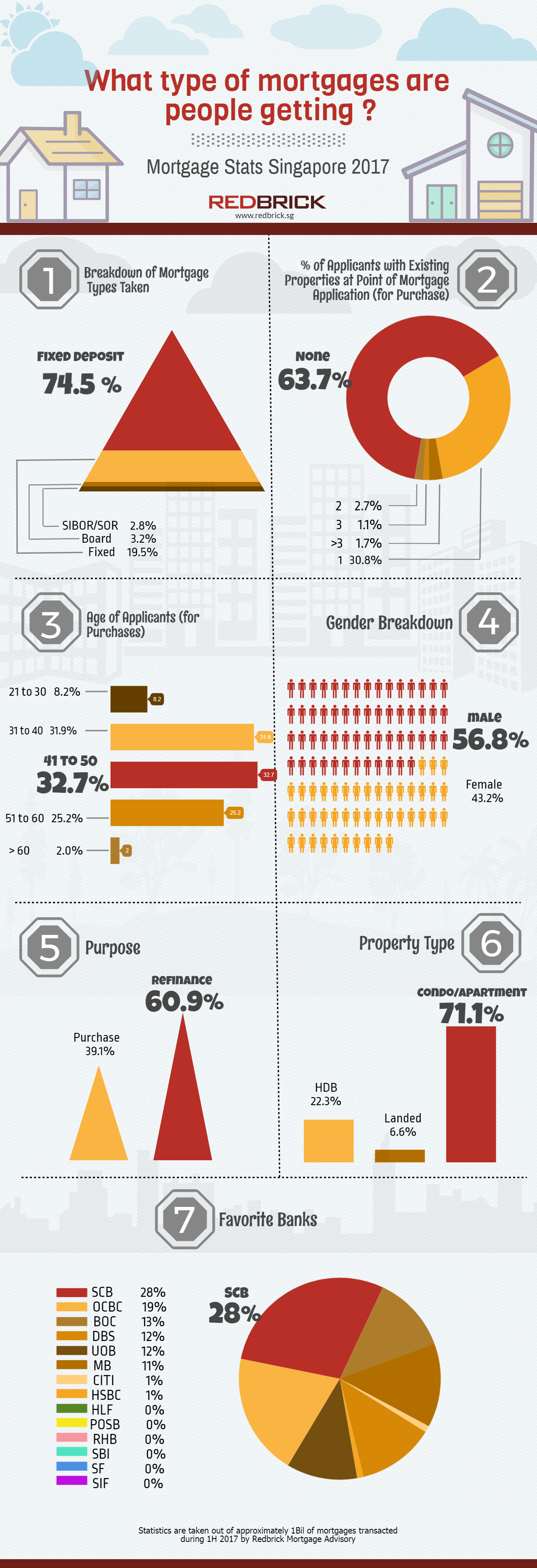

1. Mortgage preferences

Fixed deposit mortgages hold the lion’s share at 74.5%. Pegging interest rates to a bank’s fixed deposit interest rates, this mortgage type is currently offered by the 3 local banks (UOB, DBS and OCBC) along with Maybank and Standard Chartered Bank. Instead of the 6-12 months FD rates that most are more familiar with, the more obscure 18, 36, and 48-month rates are used.

Fixed mortgages, which remain popular for the stability and ease of mind they afford property buyers, follow behind at 19.5%. Interest rates stay the same during the loan’s lock-in period (1-5 years depending on the bank of choice).

Board and SIBOR/SOR mortgages, however, see significantly less takers, at 3.2% and 2.8% respectively, as these are mortgages that have floating interest rates subject to the banks and foreign exchange rates (USD). The trend is going in a different direction as opposed to a few years back where SIBOR/SOR was the mortgage package of choice.

2. Number of properties owned

If you thought that most mortgagors are seasoned property investors and acquirers, you’d be pretty surprised! Instead, many (63.7%) were first-time buyers or homeowners who have decoupled or sought to do so (this is typically done in order to purchase more property). With ABSD in full force, this is not exactly surprising. Having to pay a large premium for property purchase will erode any potential investment upside.

In contrast, only 15% of those that did own property held more than one during the point of application.

3. Age breakdown

Most mortgage applicants fall within the age bracket of 31-50 years old (64.6%), with home upgraders making up a large portion of this group. First time homebuyers buying HDB flats typically turn to HDB for their loan. It is ideal for young couples as HDB loan allows less cash upfront compared to bank loans, among other differences. With stronger financial standing, HDB upgraders seek out bank loans that offer attractive interest rates.

Loan tenures are also shorter for those who are older, which may account for the lower percentages of applicants above the age of 60, and the slightly lower 25.2% of the 51-60 age bracket.

4. Gender breakdown

More men are buying homes or property compared to women: men make up 56.8% of our mortgage applicants, with the remaining 43.2% being women. This could be due to a couple of factors at play, one being how women tend to be more conservative investors, as compared to men. Another reason could be a significant difference in spending power that results in more single men purchasing property.

The second half of 2017 could see things flipped around, however, so keep your eyes peeled for updates!

5. Reasons for mortgages

Many clients come to us for help with finding the best mortgage plans for property purchases, but an even larger number do so for refinancing (the swapping of existing home loans to others with lower interest rates).

In fact, the proportion of people refinancing loans for their existing property has increased as compared to last year (2016) – rising to 60.9% from 58% prior.

This is could be due to changes in the macro environment, such as rise in the US Fed rate, which prodded many to refinance their loans to take advantage of more attractive packages.

6. Property types

The property of choice for many of our clients are condominiums (71.1% to landed property’s 6.6%), reason being that those looking to buy HDB flats often seek loans from HDB directly. Overall, private home sales has seen an increase this year and the demand for new property is looking buoyant.

7. Banks of choice

Standard Chartered Bank was the favoured bank in the first half of this year, snagging 28% of the pie. This was largely driven by the appealing promotional rates that they offered, such as a 1% interest rate for the first year of Fixed Deposit mortgage. Another reason for their appeal is their Mortgage One scheme (only for private properties), with packages for Fixed Deposit rates or SIBOR. An interest off-set account, it helps you reduce the monthly interest on your mortgage by offsetting it with the interest from your deposits. Check it out here.

At 4th place, Standard Chartered Bank, however, currently falls behind DBS, OCBC and UOB, Singapore’s local banks, when it comes to overall market share.

Other banks that were preferred include Maybank (MB) and Bank of China (BoC). A smaller amount chose Citibank and HSBC.

__

Whether you’re new to mortgages and simply curious, or looking around for information to help you make a more informed decision, we believe that these insights will help you obtain a better understanding of the current mortgage climate.

Individual needs vary. If you need expert advice on what will work best for you, Redbrick will be happy to assist you. In the meantime, do check out our other posts for more handy tips and insights!