When it comes to your home loan, a question that separates the savers from the investors is:

“Should I pay more every month to clear my loan faster, or keep my monthly instalments low and use my money elsewhere?”

It’s a deceptively simple question, but the answer has a huge impact on your total wealth. The right choice for you depends entirely on your money mindset, your financial discipline, and a little bit of simple math.

Let’s break down the pros and cons, stripped of all the fluff.

The Case for a Shorter Mortgage Tenor (And Guaranteed Savings)

Let’s start with the most popular, conservative strategy: paying off your mortgage faster. The financial argument is crystal clear: you save a ton of money on interest.

Imagine a $1 million loan at 2% interest.

- 30-year tenor: Your monthly instalment is about $3,696.

- 20-year tenor: Your monthly instalment is about $5,058.

That’s a difference of about $1,362 per month. The longer tenor looks more “affordable,” but here’s the total cost:

- 30 years: Total interest paid = $330,560

- 20 years: Total interest paid = $214,560

By choosing a shorter 20-year tenor, you save over $116,000 in guaranteed interest. That’s money that stays in your pocket instead of going to the bank.

Other undeniable benefits of paying your loan off faster:

- You own your home sooner. Imagine being completely debt-free a decade earlier. That’s a huge mental and financial relief.

- You build equity faster. A larger portion of your monthly payment goes into the principal, boosting your net worth faster.

- You’re protected from rising rates. If interest rates spike in the future, you’re shielded from the shock because your loan is either paid off or well on its way.

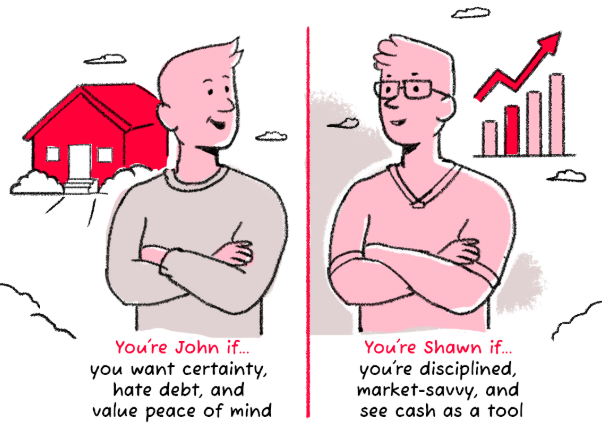

So, if your goal is peace of mind, financial freedom, and long-term savings, shortening your mortgage tenor is a powerful move.

When a Longer Tenor Could Make You Richer

Now, let’s flip the coin. What if you’re the kind of person who sees that extra $1,360 per month as an opportunity?

By extending your loan from 20 to 30 years, you free up that cash every single month. If you’re disciplined enough not to spend it on lifestyle upgrades — and instead, invest it — you could potentially come out way, way ahead.

Here’s the simple math:

To match the $116,000 in interest savings you gave up, you only need to achieve an annual return of about 1.38% on your investments over the next 30 years.

For example, John and Shawn each have a $1 million housing loan. John keeps his loan at 20 years, while Shawn extends his to 30 years.

Shawn invests the $1,360 monthly difference in a savings plan earning 3% per year.

After 30 years:

- Shawn pays $116,000 more in loan interest

- But his savings grow to $302,922

Net result: Shawn gains $186,922 even after the extra interest.

That’s… surprisingly low. In fact:

- Your CPF Ordinary Account (OA) already gives you 2.5% p.a. risk-free.

- Long-term diversified investments (stocks, bonds, REITs) have historically done far better than 1.38% p.a.

Purely from a numbers perspective, if you can get a return higher than 1.38% on your money, it may be financially smarter to extend your loan and invest the difference.

The Key Question to Ask Yourself

It all comes down to this:

Do you believe you can consistently earn more than 1.38% p.a. on your investments over the next 30 years?

- If yes: Take the longer tenor, invest the difference, and grow your wealth.

- If no: Shorten your tenor, pay off your home faster, and enjoy the guaranteed savings.

But there’s a catch: discipline matters. This strategy only works if you actually invest the difference. If that money disappears into brunches, shopping, or spontaneous travel, you’ve just paid the bank more interest for absolutely nothing.

Final Thoughts: What’s Your Money Mindset?

There’s no universal “right” answer.

But there is a right process:

- Know your numbers. Understand the interest cost difference between short and long tenors.

- Be honest about your discipline. If you won’t invest the difference, a shorter tenor is the clear winner.

- Consider your risk profile. A conservative saver who hates debt will find more peace of mind in guaranteed savings.

- Leverage guaranteed returns. Use your CPF OA’s 2.5% as a solid benchmark.

In the end, the best decision is the one that matches your financial goals and your behaviour.

So, what’s your pick? Are you the type who’d rather save $116,000 in guaranteed interest, or take the bet that you can beat 1.38% p.a. over 30 years? Your mortgage strategy says a lot about your money mindset.