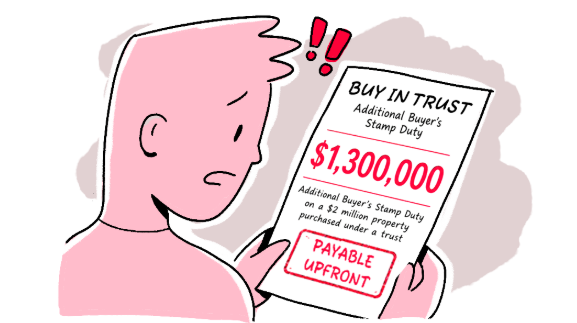

S$1.3 million.

That’s what a 65% Additional Buyer’s Stamp Duty looks like in practice — paid upfront, on a S$2 million property, the moment it’s purchased under a trust.

For many Singaporean families, this number arrives as a surprise. The logic of buying property under a trust for a child sounds reasonable on the surface: structured, protected, forward-thinking. It’s the kind of decision that signals you’re planning ahead. What it doesn’t signal — until the stamping stage — is the cost of doing so.

The question worth thinking isn’t whether a trust is sophisticated.

It’s whether the sophistication justifies the bill.

“Wealth transfer done well isn’t about the most elaborate structure. It’s about the right structure — one that actually reaches the next generation intact.”

Direct ownership: where the numbers work for most families

Singapore’s property market is built, in large part, on leverage. Over 75% of resident households live in owner-occupied homes, and the wealth most families have accumulated in real estate arrived through one consistent mechanism: a bank loan, CPF contributions, and time.

Direct ownership preserves access to all of it. You can borrow up to 75% of the property value. Your CPF Ordinary Account funds flow in without restriction. The asset appreciates, the loan amortizes, and equity builds — compounding in both directions simultaneously. This is how property wealth actually works in Singapore, and it works because of leverage.

Trust purchases sit outside this model. Because the beneficial owner — the child named in the trust — has no income and no credit history, financing is rarely available. The purchase is typically made in cash. That means the full capital is deployed upfront, with no gearing, no CPF contribution, and no amplification of returns. The asset needs to grow significantly just to offset what leverage would have delivered for free.

There is also the matter of flexibility. A direct owner can sell when the market is favorable, refinance when liquidity is needed, or pivot to a different asset if circumstances change. A trust moves more slowly by design — that’s part of its purpose — but in a market that rewards timing, that rigidity carries a real cost.

What direct ownership can’t guarantee on its own

Growing wealth and transferring it cleanly are not the same discipline. Direct ownership handles the first well. The second requires deliberate planning that ownership alone doesn’t provide.

When a property passes to the next generation without a clear structure — through inheritance or an unplanned transfer during illness — several things can go wrong simultaneously. Outstanding debt follows the asset. Legal disputes surface between beneficiaries. Creditor claims, which would otherwise be manageable, suddenly have access to family property at the worst possible moment.

The generational wealth data is sobering on this point. Research from Credit Suisse consistently shows that family wealth diminishes significantly by the second or third generation — not because the assets weren’t there, but because the handover was unplanned. The property existed. The governance around it didn’t.

This is not an argument for trust. It’s an argument for the intent. A well-drafted will, a properly structured estate plan, and sound legal counsel at the right life stage can address most of these risks for a fraction of what a trust costs. The gap direct ownership leaves is real — but it doesn’t require a trust to close it.

| 💰 What the numbers actually show 65% ABSD on a S$2M trust purchase = S$1.3M in stamp duty before the asset earns a single dollar. For direct purchase under a Singapore citizen’s name, the first-property rate is 0%. That gap isn’t a policy detail. It’s the entire argument. |

The complexity trusts carry — and who it’s actually for

A trust is not a bad instrument. For the right family, in the right circumstances, it does something no other structure can: it separates the timing of ownership from the timing of benefit. The asset is held. The beneficiary is named.

However, the transfer — when it happens, how much, under what conditions — is governed by the trust deed, not by circumstance or grief or a court’s interpretation of an ambiguous will.

At age 35, and not before. Only after completing a degree. Proportionally, across three children, based on need. These are conditions a trust can enforce. For families managing substantial multi-generational wealth, blended family dynamics, business succession, or assets across multiple verticals, that control is worth paying for. It addresses a category of risk that simpler structures genuinely cannot.

The difficulty is that Singapore’s policy environment has made that control very expensive. The 65% ABSD applies to all residential properties purchased under a trust, without exception and without regard to intent. It applies whether the trust is designed for estate planning, asset protection, or legacy distribution. Anti-avoidance rules have also been strengthened, meaning trusts perceived as primarily tax-motivated face additional scrutiny.

Ongoing costs compound the entry price. Trustee fees, legal administration, and the reduced liquidity of trust-held assets create a friction that accumulates quietly over years. For most Singaporean households, the structure costs more to run than the problem it solves is worth.

The families for whom a trust genuinely earns its complexity are those with substantial assets, layered succession needs, and the professional infrastructure to manage it properly.

So which structure actually fits your situation?

The most useful question isn’t “trust or direct ownership?” It’s a more specific one: what problem are you actually trying to solve?

If the goal is building property wealth — growing equity, leveraging CPF, creating an asset base to upgrade from over time — direct ownership is the answer for the vast majority of Singaporean families. The cost efficiency is real, the financing access is genuine, and the flexibility to adapt as life changes is something a trust cannot offer.

If the goal is controlling how that wealth transfers — protecting it from mismanagement, structuring it across a complex family picture, or ensuring it arrives at the right time rather than the wrong one — then a trust may be the right instrument. But only if the asset base justifies the entry cost, and only with clear-eyed accounting of what the 65% ABSD actually represents.

For most families, the practical answer sits between the two. Direct ownership for growth. A well-structured estate plan to govern the transfer. Legal counsel engaged early enough to make it deliberate rather than reactive. That combination addresses the real risk without the architecture of a trust and the bill that comes with it.

The question that clarifies everything

Before settling on a structure, it helps to separate two things that often get mixed: the plan to build wealth, and the plan to transfer it.

“If the asset I’m building today had to change hands tomorrow — unexpectedly, imperfectly, under pressure — what would happen to it?”

If you can answer that with confidence, the structure you’ve chosen is doing its job. If the answer is unclear — if the honest response involves uncertainty about debts, disputes, or timing — that’s the gap worth addressing. Not necessarily with a trust. But with something.

Singapore’s property market rewards people who plan both sides of the equation: the accumulation and the handover. Most families spend years optimizing the first and very little time on the second.

A structure isn’t a guarantee. But the absence of one is a risk that compounds quietly, across years, until it doesn’t.