There was a time when a successful BTO application in a good location felt like winning the lottery. You’d buy low, wait for the five-year Minimum Occupation Period (MOP) to pass, and then sell high. These windfalls, often in the 6-figure range, were the rocket fuel that helped many young couples launch into the private property market.

But here’s the reality check: that “BTO lottery” is quickly coming to an end.

New regulations like the Prime and Plus flat models, with their longer 10-year MOPs and subsidy clawbacks, are designed to kill that lottery effect. The resale windfall is shrinking, and for a new generation, the entry into the private market is becoming increasingly difficult.

So, how are more and more young Singaporeans buying private property in their mid-to-late 20s, barely out of university?

The answer isn’t a secret, but it’s a reality few want to talk about.

The New Math to Enter the Private Market

Let’s look at the numbers for a typical young couple. Say you and your partner earn a solid combined income of $16,000 per month. You have your sights set on a modest $2 million condo.

Even with that healthy income, the upfront outlay is significant. We’re talking about a downpayment of at least $500,000, of which $100,000 must be in cash. Add in stamp duties and other legal fees, and the total upfront cost can easily be close to $600,000.

Now, do the math. If you’re saving a combined $4,000 a month—a very disciplined, healthy savings rate—it would still take you 12 to 15 years just to save up for the downpayment. And that’s before factoring in big life events like kids, career changes, or emergencies.

The Unspoken Advantage: The Rise of Intergenerational Wealth

Meanwhile, a growing number of young professionals are entering the private market a decade earlier, with the financial support of their parents.

Imagine a similar couple, but their parents have unlocked $300,000 to $400,000 of their home equity to help them with the downpayment.

Suddenly, their timeline shrinks from over a decade to just a few years. They can enter the market in their mid-20s, building equity and capital appreciation while their peers are still years away from reaching their savings goals.

This isn’t a new phenomenon, but it is becoming increasingly common. The gap between those with intergenerational wealth and those without is widening, creating a clear divide in the Singapore private property market.

Closing the Gap: Early Planning Is Non-Negotiable

This isn’t a “have-and-have-nots” story meant to discourage you. It’s a reality check.

The truth is, the era of easy, almost passive, wealth creation from property is over. If property is part of your long-term wealth plan, meticulous and early planning is no longer a choice—it is non-negotiable.

For those without parental support, it means:

- Starting early: You must begin saving and planning the moment you start your first job.

- Making strategic moves: Your first property is no longer just a home; it’s a strategic asset. You must choose it wisely.

- Diversifying your investments: Relying on property alone is a risk. You need to grow your wealth through other channels, like stocks and ETFs, to build up your own capital.

Here’s how you can prep ahead:

1. Financial Clarity: Honesty is the Best Policy

You cannot plan for a multi-million-dollar asset if you don’t even know where your cash goes every month. The first, and hardest, step is being honest with yourself about your income and your expenses.

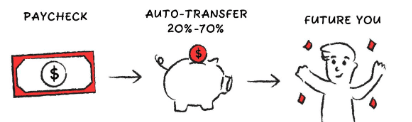

- Know Your Flow: If you’re not someone who tracks every dollar, use the “pay yourself first” method. As soon as your salary hits your bank account, immediately transfer your savings—aim for a realistic 20% to 70% of your income into a separate investment or savings account before you spend anything.

- The Power of Review: Make it a habit to review your finances every few months. This isn’t about guilt; it’s about course correction. A regular review helps you identify spending creep, check if your savings rate is on track, and make small, painless adjustments before they become big problems.

2. Mindset Shift: Stop Buying a “Forever” Home

It’s common for young couples to buy their first home, spend S$100,000 on a gorgeous renovation, and imagine living there forever. But the reality is that many end up selling within five to eight years due to a job change, new child, or a desire to upgrade.

Instead of asking, “Do I want to live here forever?” ask yourself this: “Will this property give me options later?”

A good first property should serve your financial goals, not just your immediate comfort. Focus on flexibility:

- Resale Demand: Does the property have good resale demand for a quick exit if you need to upgrade?

- Rental Viability: Could you rent it out easily if you decide to buy a second property and move?

- Renovation Cost vs. Value: Are you spending too much on a renovation that won’t add any value to the next buyer? Keep emotional spending low and strategic spending high.

Your first property should be a stepping stone to your second, not a final destination.

3. Diversification: The Hidden Cost of Cash

You already know that leaving money in a low-interest bank account means it loses value over time thanks to inflation. The worst investment you can make is doing nothing.

You need to put your money to work, and you don’t need to be a market genius to start:

- Dollar-Cost Averaging (DCA): This is a simple, disciplined approach. Commit to putting a fixed amount each month into broad market investments like an S&P 500 ETF or a World ETF. This smoothens out market ups and downs and builds long-term discipline.

- The Compounding Advantage: Even at a modest 5% annual growth rate, the difference over time is massive. If you invest S3,000 a month for 10 years, your money could grow to approximately $465,000. Keep that same S3,000 in a typical bank account, and you only have $360,000. That’s a S$105,000 in opportunity cost.

- The Cash Buffer: Always keep some cash aside. When the market drops by 10% to 20%, that is a potential buying opportunity.

Ultimately, whether you get to that $2 million condo in 8 years or 15 years, the journey is defined by the work and planning you put in today. The game has changed, but the opportunity remains for those who are prepared to play by the new rules.