“UK property giving 7% yield.”

“Japan rental income very strong.”

“Entry price cheaper, easier to start.”

You’ve heard some version of this — at a seminar, over dinner, in a WhatsApp group where someone just got back from a property roadshow. And on the surface, the arithmetic seems to hold. Higher yield, lower entry price, stronger upside. It sounds like a rational case.

The problem isn’t the logic. It’s the inputs. The numbers being quoted are gross yields, pre-tax, pre-cost, pre-currency conversion, measured in a foreign market by someone who benefits from you buying. The number that actually matters — what you keep, in SGD, after everything — is rarely on the slide.

“The yield figure is the beginning of the analysis. For most investors who buy overseas, it ends up being the end of it.”

The appeal is real — so is the risk sitting behind it

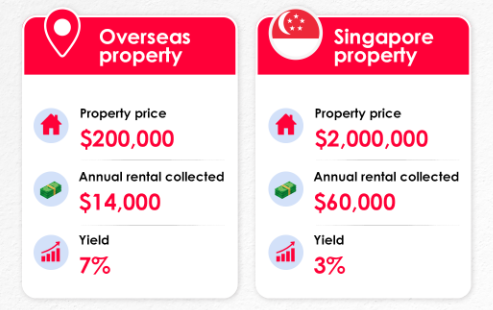

Singapore’s private residential yields sit at around 2% to 4%, according to URA and CBRE data. Against that baseline, markets offering 6% or 7% gross yields are not imaginary. The numbers exist. The gap is real.

Lower entry prices in certain overseas markets also matter, particularly for investors earlier in their wealth-building journey. A S$200,000 apartment in a regional city allows participation in property investment at a quantum that Singapore doesn’t offer. For building experience and diversifying across geographies, there’s a rational argument.

What changes the calculation is what comes next. Gross yield is a starting point, not an outcome. Between that headline number and what actually lands in your bank account sits a chain of costs and risks, each one individually manageable, but collectively capable of transforming an apparently attractive investment into an indifferent or negative one.

What Singapore’s 3% yield is actually telling you

Singapore’s residential yield is often described as low. A more accurate description is transparent. What you see is what you get: a market with a clear legal framework, structured financing, CPF accessibility, and an exit pool that includes HDB upgraders, permanent residents, and international buyers. Vacancy risk is real but bounded. Currency risk doesn’t exist — you’re already in SGD.

There is no withholding tax on rental income for Singapore residents. The conveyancing process is standardized, with reliable timelines and clear recourse. Property tax is predictable. The rules don’t change mid-investment based on foreign policy shifts or local political decisions you have no ability to monitor or anticipate.

None of this eliminates risk. Prices can fall. Tenants leave. Interest rates move. But these are known, domestic, legible risks — the kind you can model, plan for, and manage. The 3% yield, understood in this context, is the return on an asset where the variables are visible. The relevant comparison isn’t 3% versus 7%. It’s 3% with known risk versus 7% with unknown risk. That is a fundamentally different equation.

| 💰 What the numbers actually show A 7% gross yield in the UK, after 20% withholding tax, 10–15% management fees, vacancy allowance, and currency drag, can compress to an effective return of 3–4% in SGD terms — before maintenance. Singapore’s 3% yield, held in your home currency, with no foreign tax exposure and a liquid exit market, starts to look less modest by comparison. |

Where overseas deals quietly come apart

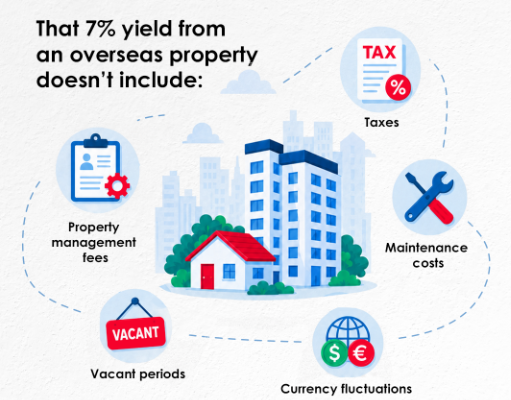

The mechanism by which overseas property investments fail is rarely dramatic. It’s cumulative. Each variable compresses the return a little further, until the investment that looked like 7% is delivering something closer to 2% — or less, or negative — in the currency you actually spend.

Withholding tax on rental income ranges from 20% to over 40% in many markets, depending on residency status and tax treaty arrangements. Management fees for overseas properties, where you cannot self-manage, typically run 8% to 15% of gross rent. Vacancy periods in markets where you have no local network and limited visibility into demand cycles are harder to fill and longer to recover from. Currency movement is unpredictable and non-negotiable: SGD has strengthened meaningfully against the Malaysian ringgit, the Japanese yen, and the British pound over multi-year periods, compressing SGD-converted returns even when the local investment performed adequately.

The Johor Bahru experience is the clearest recent illustration. Projects like Forest City were marketed aggressively to foreign buyers on the basis of projected growth and rental demand. Supply significantly exceeded local absorption capacity. Bank Negara Malaysia reported tens of thousands of unsold residential units across Malaysia in subsequent years, with Johor among the most severely affected regions. The exit that investors planned — selling to the next buyer at a higher price — required another foreign buyer willing to pay more than they had. That buyer pool did not materialize.

The pattern is not unique to Johor. It emerges anywhere that developer supply is driven primarily by foreign investor appetite rather than local occupier demand. When the marketing stops, the demand stops with it.

Diversification or just risk in a different postcode?

The most common rationale offered for overseas property investment is diversification. It’s a reasonable instinct. Concentrating all your assets in a single market carries its own risks.

The question worth examining is whether another property — in a different country, with its own currency, legal system, tax regime, and demand dynamics — actually diversifies your portfolio in a meaningful sense, or whether it simply relocates the concentration while adding several new categories of risk: execution risk, currency risk, political risk, and the operational burden of remote management.

For most Singaporean investors, whose primary asset is already residential property, adding a second property overseas increases total property exposure. It does not reduce it. If genuine diversification is the goal, the more direct routes are through REITs, which offer income exposure across geographies and asset classes without the operational complexity; equities, which provide growth exposure uncorrelated to a single property market; or simply increasing liquidity, which preserves optionality when better opportunities appear.

Overseas property can be a legitimate part of a well-structured portfolio. For an investor who genuinely understands the target market, has verified local demand dynamics, has accounted for every layer of cost and tax, and has modelled the return in SGD terms across a realistic holding period — the investment can make sense. The difficulty is that very few people going into overseas property have done that work. Most have seen a yield figure and a price point. That’s not a portfolio strategy. It’s a starting point that needs a great deal more analysis before it becomes one.

The question most investors don’t ask until it’s too late

Before committing capital to an overseas market, there is one question that cuts through most of the noise:

“What is my actual return, in SGD, after tax, after costs, after currency, across my intended holding period — and what does my exit look like?”

Not the gross yield. Not the developer’s projected appreciation. The net figure, in your currency, on a realistic timeline, with a specific buyer in mind at the end of it.

Most investors who have done this calculation find that the gap between the overseas investment and a Singapore one narrows considerably. Some find it disappears. A few find the overseas market still wins on the numbers, and for those investors, with genuine market knowledge and a clear exit strategy, the case is defensible.

The discipline is in doing the calculation before you buy, not after. Yield is what a market offers. Return is what an investor earns. They are not the same number, and the distance between them is where most overseas property investments are either won or lost.