When you are planning to buy an HDB flat or an Executive Condominium (EC), one of the first questions that comes up is simple: how much can you actually afford to repay each month?

The Mortgage Servicing Ratio (MSR) sits right at the centre of that decision, shaping how much you can borrow, how heavy your monthly instalments may be, how much CPF you may want to use, and whether your chosen BTO flat, resale HDB, or Executive Condominium (EC) fits your finances in a way that still feels sustainable in Singapore’s housing market.

Understanding how MSR works is the first step to knowing what you can realistically afford, so let’s look at how the rule applies and how it affects your housing loan options in Singapore.

1. What Is the Mortgage Servicing Ratio (MSR) in Singapore?

The Mortgage Servicing Ratio (MSR) is a housing loan rule that applies to the purchase of an HDB flat or an Executive Condominium (EC) bought from a developer.

In Singapore, MSR is capped at 30% of your gross monthly income. This means only part of your monthly income can go towards your home loan repayment.

MSR is often confused with TDSR, though they measure different things. MSR looks only at your monthly home loan repayment for covered housing purchases, while TDSR looks at your total monthly debt obligations across all loans.

Also read: TDSR Singapore: A Complete Guide for Homebuyers and Property Owners

1.1. How MAS defines the Mortgage Servicing Ratio

The Monetary Authority of Singapore (MAS) defines MSR as the share of a borrower’s gross monthly income used to repay the monthly mortgage for loans covered by the rule.

- In practical terms, it is a monthly affordability check that helps determine whether the repayment fits your income at a level considered manageable.

- In simpler terms, MSR answers one question: how much of your monthly income can safely go into your housing loan?

Key takeaways:

- MSR focuses on monthly repayment, not just property price.

- A buyer may have enough for the downpayment and still not meet the MSR limit.

- For HDB flats and new ECs, MSR is often one of the first affordability limits that shapes the loan amount.

Also read: A Singaporean Guide to Buying your First HDB in Singapore

1.2. Why the MSR rule exists

MSR forms part of Singapore’s broader housing-finance framework. Its purpose is to support prudent borrowing by limiting how much of your income is tied up in mortgage repayments. This helps keep a home financially manageable alongside other regular expenses and financial commitments. MAS describes MSR and TDSR as part of Singapore’s macroprudential safeguards for the property market.

Why this matters for first-time buyers

For first-time buyers, MSR keeps the focus on repayment sustainability over time, not just purchase eligibility at the start.

This is especially relevant when you are:

- looking at a larger resale HDB flat

- considering a higher-priced EC launch

- trying to stretch your budget based on savings alone

- comparing different loan scenarios with CPF and cash contributions

Image: 4 Key Factors That You Must Know When Assessing Your Loan Eligibility

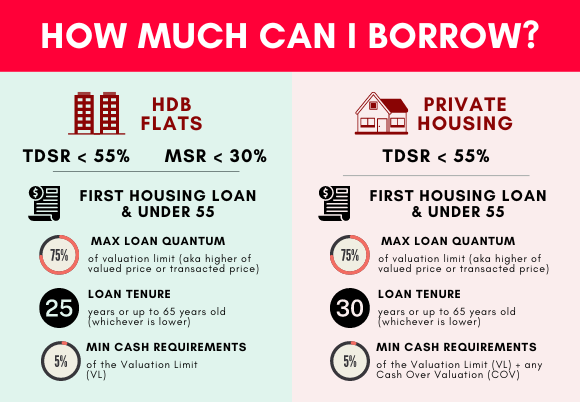

2. What Is the Current MSR Limit in Singapore?

2.1. MSR limit for HDB housing loans

If you are buying an HDB flat, the MSR cap remains 30%.

This applies whether you take an HDB concessionary loan or a bank loan for the HDB purchase. Alongside MSR, the broader HDB financing framework also matters: the HDB concessionary interest rate remains 2.6%, while the maximum loan-to-value (LTV) for eligible HDB housing loans is up to 75%.

Why passing MSR does not mean full approval yet

Passing MSR gives you one green light, though it does not mean the full approval process is complete. Your final loan outcome still depends on factors such as:

- your age

- your loan tenure

- your income documents

- your credit profile

- your wider debt position under TDSR

- the bank’s own underwriting assessment

That is why you can stay within the 30% cap and still receive a smaller approved loan amount than expected.

2.2. MSR limit for Executive Condominiums

If you are buying a new EC from a developer, the MSR cap is also 30%.

This is where many buyers trip up. Because ECs are often compared with private condominiums in terms of product and pricing, it is easy to assume the financing treatment works the same way from day one. In reality, at the purchase stage, ECs remain subject to public housing style affordability rules such as MSR.

Why EC buyers often misread the financing rules

If you are considering an EC, these are the points that usually catch buyers off guard:

- you may compare it with a private condo based on layout, facilities, and price

- your financing treatment at purchase stage is still stricter than standard private housing

- you often need to think about MSR and TDSR together, not just one ratio in isolation.

2.3. What happens if your mortgage exceeds the MSR?

If your estimated monthly mortgage repayment goes above the 30% MSR cap, the current loan structure falls outside the allowed limit. That usually leads to one or more of these outcomes:

- a lower loan quantum

- a higher upfront payment using CPF or cash

- a different loan structure, including a longer eligible tenure

- a lower property budget

Common reasons buyers cross the MSR line

If you find yourself above the MSR cap, the reason is usually one of these:

- the property price is too high relative to your current income

- the loan tenure is too short, which pushes up your monthly instalments

- your repayment estimate is based on rough budgeting rather than a professional assessment

- another property loan is already being counted in your repayment profile.

| Property type | Does MSR apply? | Current cap | Does TDSR also apply? | Typical financing route |

| HDB flat (BTO/Resale) | Yes | 30% of gross monthly income | Yes, where applicable | HDB loan or bank loan |

| New EC from developer | Yes | 30% of gross monthly income | Yes | Bank loan |

| Private condo | No | Not applicable | Yes | Bank loan |

| Landed property | No | Not applicable | Yes | Bank loan |

Table: Current MSR rules at a glance

If you want to test how these limits translate into actual monthly repayments, use Redbrick’s The Best Mortgage Calculator in Singapore to connect well with this part of the journey.

3. How to Calculate the Mortgage Servicing Ratio

Once you know the MSR limit, the next step is to work out what that means for your own monthly repayment ceiling. The basic calculation is simple enough to do on paper.

The more important part is understanding how banks read that number when assessing your home loan. Getting an estimate gives you a starting point on the loan quantum, while the bank’s assessment determines how much you can actually borrow.

3.1. MSR formula explained

| MSR = Monthly mortgage repayment ÷ Gross monthly income × 100% |

You can also use the formula in reverse to estimate the maximum monthly repayment your income can support.

- If your gross monthly income is S$8,000, your monthly repayment ceiling is S$2,400

- If your gross monthly income is S$10,000, your monthly repayment ceiling is S$3,000

These figures give you a quick view of how much room you have before other lending factors come into play.

| What counts as the monthly repayment in planning terms When you estimate MSR for yourself, it is easy to treat the monthly repayment as a rough number from a calculator or property listing. In practice, banks assess affordability using formal loan assumptions and debt-servicing rules. → That means the same income can still lead to different outcomes depending on the interest rate used, the loan tenure, and your overall debt profile. A useful way to think about it is this: • your own estimate tells you whether a property feels broadly within reach • the bank’s assessment decides whether the repayment fits the regulatory framework • the gap between the two is often where buyers realise their budget is tighter than expected |

3.2. Example MSR calculation using monthly income

The easiest way to understand MSR is to see how it works across different buyer situations.

| Example 1: Single borrower If you earn $6,000 a month: • Gross monthly income: $6,000 • Maximum housing repayment (MSR): $1,800 This means your home loan repayment should stay around $1,800 per month or less. Assuming: • 4% interest rate • 25-year loan tenure Your estimated maximum loan may be around: ≈ $340,000 loan This could support a property price of roughly: ≈ $450,000–$460,000 (depending on downpayment and CPF) |

| Example 2: Dual-income household If your combined household income reaches $10,000 a month: • Combined gross monthly income: $10,000 • Maximum housing repayment (MSR): $3,000 This means you can support a higher monthly instalment. Assuming: • 4% interest rate • 25-year loan tenure Estimated maximum loan: ≈ $570,000 loan This could support a property price of roughly: ≈ $760,000–$780,000 (depending on downpayment and CPF) |

| Example 3: Same income, different affordability outcome Two households earn the same income, though existing liabilities can reduce how much they can borrow. Household A: Minimal debt • Income: $10,000 • Housing repayment limit: $3,000 • Other monthly debt: $0 Estimated borrowing capacity: ≈ $570,000 loan Household B: Existing debt • Income: $10,000 • Housing repayment limit under MSR: $3,000 • Existing car loan, credit card and personal loan: $3,100/month Because TDSR considers total debt obligations, the housing repayment allowance becomes smaller. Estimated borrowing capacity: ≈ $450,000 loan → What this shows Even with the same income, the final loan amount can change depending on: • existing debts • loan structure • bank affordability assessment That is why two buyers with the same income profile can walk away with very different loan approvals. |

3.3. What income counts toward MSR

For most salaried workers, the income used for MSR is straightforward: your gross monthly salary.

Things get more complex when your income changes from month to month. If part of your income comes from commission, bonuses, freelance work, or other variable sources, MAS states that financial institutions use the average monthly variable income earned over the past 12 months for debt-servicing assessment.

For example:

- If your fixed salary is $4,000, and your commission over the past 12 months averages $1,000 a month, the bank may assess your monthly income as $5,000, not just your fixed salary.

Income situations that are assessed differently

- Variable-income earners

If your pay changes from month to month, the bank usually looks at your average income over time, rather than your highest recent month. - Self-employed applicants

If you run a business or work for yourself, the bank usually looks more closely at your Notice of Assessment (NOA), tax records, and supporting proof of income to decide what income can be recognised. - Joint borrowers

If you apply with another borrower, both incomes may be counted together. That increases the total monthly income used for the MSR calculation.

Proof of documents for income and loan assessment

Banks do not assess your income solely based on your declaration. They look for proof of income before assessing your loan application. That includes the following:

- payslips

- CPF contribution history

- Notice of Assessment (NOA)

- bank statements

- commission statements or other supporting income records

This is why two buyers with similar earnings may still be assessed differently. One may have clear paperwork with records of regular income, while the other may only track irregular income or sources that are harder to verify.

4. How the Mortgage Servicing Ratio Affects How Much You Can Borrow

By the time you reach this stage, MSR has already influenced more than your repayment limit. It shapes several decisions buyers make during the house hunt — from the price range to how they structure their financing.

Rather than acting as a single approval rule, MSR becomes part of the broader framework that determines how comfortably a home fits into your monthly finances.

4.1. How MSR shapes your home budget

When buyers begin viewing flats or EC projects, the focus often starts with the property price. MSR shifts that perspective toward the monthly commitment required to hold the property.

This is why two properties with similar prices can feel very different financially once the repayment structure is considered.

Several factors influence how the property budget translates into the monthly repayment:

- the loan tenure chosen

- the interest rate used by the bank

- the proportion of the purchase funded through CPF or cash

- the total loan amount required

Hence, buyers often adjust their search criteria after running the numbers. A property that initially appears affordable based on price alone may feel less comfortable once the repayment is viewed against monthly income.

4.2. How CPF usage influences your monthly cashflow

CPF plays a significant role in how the monthly repayment is funded, though it does not change the MSR calculation itself.

For eligible property purchases, CPF Ordinary Account (OA) savings may be used for:

- downpayment

- monthly housing repayments

- stamp duties

- legal fees

This gives buyers flexibility in managing how much of the repayment comes from cash versus CPF.

| CPF usage can influence | CPF usage does not change |

| How much cash you pay each month | The MSR formula |

| How the purchase is funded upfront | Your repayment ceiling |

| The balance of cash vs CPF used for housing | Loan approval rules |

The CPF trade-off

Using CPF for housing can make monthly finances feel lighter in the early years of ownership. At the same time, CPF used for property will generally need to be refunded with accrued interest when the property is sold.

Thus, some buyers aim to keep a balance between CPF usage and cash payments, especially if they want to preserve OA savings for future investment or financial needs.

Also read: Don’t Get Caught: The Hidden Rules of Using CPF for Your Home

4.3. Why loan structure matters as much as the property price

Even when two buyers purchase the same type of property, the structure of the loan can lead to different financial outcomes.

| Key elements of the loan structure include: • loan tenure • interest rate package • fixed vs floating rate choices • amount of upfront downpayment Loan tenure in particular has a noticeable effect on the monthly repayment pattern. |

A longer tenure generally spreads repayments over more years, which reduces the monthly instalment. Whereas, a shorter tenure concentrates the repayment over shorter duration, increasing the monthly instalment but reduces the total interest paid.

Sometimes, adjusting the loan structure can make home repayments more manageable than searching for another property that fits the bill altogether.

Redbrick’s mortgage calculators can help illustrate how changes in interest rate and tenure affect repayment patterns across different loan scenarios.

5. Mortgage Servicing Ratio (MSR) vs Total Debt Servicing Ratio (TDSR)

The next question you should ask is whether your debt profile affects how much you can borrow. Here’s where the Total Debt Servicing Ratio (TDSR) becomes relevant. While MSR looks at your home loan repayment, TDSR looks at your overall monthly liabilities.

5.1. Key differences between MSR and TDSR

| Mortgage Servicing Ratio (MSR) | Total Debt Servicing Ratio (TDSR) | |

| What it measures | Your monthly home loan repayment against your gross monthly income | Your total monthly debt obligations against your gross monthly income |

| Current cap | 30% | 55% |

| Applies to | HDB flats and ECs bought from developers | All properties |

| What it captures | Housing loan only | Housing loan + car loan + credit cards + personal loans + other debt |

| What it restricts most directly | Your monthly mortgage affordability | Your overall debt affordability |

| Where it matters most | When you are buying an HDB flat or new EC | When you are taking on a property loan and already have other debt obligations |

| Typical outcome if you exceed it | Your home loan structure may need to be reduced or reworked | Your total borrowing capacity may be reduced, even if the home loan alone looks manageable |

5.2 When MSR applies vs when TDSR becomes the deciding factor

| If your main issue is… | The tighter rule is usually… | What it means for your loan |

| Your housing instalment alone feels too high for your income | MSR | Your property budget or loan structure may need to be adjusted |

| Your overall monthly debt load is already heavy | TDSR | Your borrowing room may shrink even if the home loan itself looks manageable |

| You are buying an HDB flat or new EC with few other debts | Often MSR | The housing repayment itself is likely to be the main limit |

| You already have a car loan, personal loan, credit card debt, or another property loan | Often TDSR | Existing debt may reduce how much home loan you can take |

| Your income looks strong, but the approved loan still comes back lower than expected | MSR or TDSR | The tighter ratio in your profile is usually the one driving the outcome |

5.3. How banks assess both ratios

Banks do not choose whichever ratio gives you the easier outcome. They assess all applicable rules together and look at your profile as a whole, including your housing instalment, other debt obligations, income, and loan structure.

The tightest active ratio becomes the real bottleneck on how much you can borrow. That is why one borrower may be limited by MSR, while another with the same income may be constrained more by TDSR.

Why some borrowers pass one ratio and fail the other

- You may pass TDSR and still fail MSR if your home loan instalment alone is too heavy for your income.

- You may also pass MSR and still fail TDSR if you already carry other monthly debts such as a car loan, personal loan, or large credit card commitments.

If you are buying an HDB flat or a new EC, you are often being tested against both at the same time.

Also read:

6. MSR Exemptions in Singapore

The Mortgage Servicing Ratio applies mainly to housing loans used to purchase an HDB flat or an Executive Condominium from a developer. Outside these purchase scenarios, MSR may not apply. Instead, banks typically assess affordability under other debt frameworks, depending on the type of property and the loan structure.

6.1. Who qualifies for exemption

MSR exemption is not a general category for buyers. It usually appears in specific loan situations, particularly when the loan is not for a new purchase.

Examples include:

- Refinancing certain existing HDB or EC housing loans, especially older loans taken before the MSR framework was introduced

- Loan restructuring or repricing where the borrower remains the owner-occupier and the transaction does not involve a new property purchase

- Certain cases where the loan purpose is not tied to acquiring a new HDB or EC unit

MAS materials emphasise that these situations are evaluated case by case by banks, and confirmation is typically needed from the bank or mortgage advisor.

6.2. Situations where MSR does not apply

MSR does not generally apply when the property purchase falls outside the public housing purchase framework.

Common examples include:

- Private condominium purchases

- Landed property purchases

- Some refinancing scenarios for existing housing loans

In these cases, affordability is typically assessed using TDSR, which considers the borrower’s total monthly debt obligations rather than just the housing instalment.

What “MSR does not apply” actually means

If MSR does not apply to your loan, it does not mean the loan is free from affordability limits. Instead, another debt rule usually becomes the main constraint.

Key points to remember:

- Property loans outside the MSR scope are commonly assessed under TDSR

- TDSR considers all monthly debt obligations, including car loans, credit cards, and personal loans

- MAS caps TDSR at 55% of gross monthly income for property loans

No MSR does not mean unlimited borrowing. It usually means the loan is assessed under TDSR instead.

Also read:

- Decoding the Guidelines for Buying Private Property in Singapore

- How To Get A Mortgage And Finance Your Property Purchase

7. What to Do If You Don’t Meet the MSR Limit

If you do not meet the MSR limit, the next move is not to guess. It is to work through the parts of the purchase that actually change affordability.

A tighter result usually points to one of four things: income, loan size, repayment structure, or property choice. Here is a step-by-step format to look at it.

Step 1: Check whether your recognised income is being assessed correctly

Start with income. Even a small shift here can change your repayment ceiling.

This matters if:

- you are applying alone instead of with an eligible joint borrower

- your income has recently increased

- you earn variable income and now have a stronger 12-month track record

- you are self-employed and your documents now show clearer, more stable earnings

When this changes the outcome

- Single borrower → joint borrower

- Weaker 12-month record → stronger 12-month record

- Before pay raise → after pay raise

- Loose self-employed records → stronger tax and income documentation

Step 2: Reduce the loan amount you need

If the monthly instalment is too high, reducing the loan amount is the fastest way to bring it down.

That usually means:

- putting down a higher cash downpayment

- using more CPF upfront for eligible housing costs

- buying a lower-priced flat

What this changes for you

A smaller loan means:

- a lower monthly instalment

- less pressure on your budget each month

- a better chance of fitting within the allowed repayment range

Step 3: Review whether a longer tenure helps

If your loan structure allows it, extending the tenure can reduce the monthly instalment and improve your affordability result.

This is helpful when:

- your income is steady, though your monthly ceiling is tight

- the property is within reach, but the instalment is just above the allowed range

- you want to reduce monthly pressure without changing the property immediately

What to keep in mind

A longer tenure can:

- lower the monthly instalment

- make the loan fit more comfortably each month

- increase the total interest paid over time

Step 4: Reassess the property, not just the loan

Sometimes the MSR result is telling you that the property target is too ambitious for your current stage, even if it feels within reach.

That is where housing strategy matters more than loan tweaking.

Common re-evaluation paths

- Larger resale HDB → smaller resale HDB

- New EC launch → HDB alternative

- Aggressive budget → more conservative purchase

- Immediate purchase → delayed purchase after higher savings accumulation

Step 5: Decide whether now is the right time to buy

If several adjustments are needed at once, the better move may be to step back, strengthen your numbers, and return later with a stronger buyer profile.

This usually makes sense when:

- your income is still rising

- your cash savings are not yet comfortable

- your CPF buffer feels too thin

- you would need to stretch across too many fronts just to make the purchase work

| If the issue is… | Start with… |

| Income too tight | Add an eligible joint borrower or wait for stronger income records |

| Monthly instalment too high | Reduce the loan amount |

| Instalment slightly above limit | Review tenure options |

| Budget feels too stretched overall | Change the property target |

| Too many weak points at once | Delay the purchase and build a stronger base |

Turn the Numbers Into a Smarter Home Loan Decision

MSR gives you a strong starting point, though buying a home rarely comes down to one number alone. Your final loan decision still depends on how your income, CPF usage, repayment structure, and bank requirements come together.

That is why many buyers choose to speak with a mortgage advisor before committing to a loan package. A good advisor helps you see the bigger picture, compare your options more clearly, and understand how the financing choice fits your budget over time.

With Redbrick Mortgage Advisory, you can get help to:

- compare home loan options across different banks

- understand how MSR, TDSR, and other loan rules affect your profile

- plan your loan structure more clearly before you commit

- work through CPF and cash considerations with greater confidence

If you are preparing to make a property purchase, speaking with a Redbrick mortgage advisor can give you a clearer view of what fits your finances and what makes sense for your next move.